2019 TLWM Annual Outlook

Submitted by TLWM Financial on December 19th, 20182018 has been a challenging year for investors as volatility returned with a bang after being almost completely absent in 2017 when stocks roared higher by almost 20% as measured by the S&P 500 (YCharts). Through December 14th the S&P 500 is down almost 3% after enduring two corrections of 10%+ throughout the year (YCharts). Volatility like this can be uncomfortable even for the most seasoned investor and keeping focused on your long-term goals and objectives is critical when headlines constantly remind us of everything we should be worried about. These headlines included many factors that are likely to be talked about throughout 2019 including trade, the yield curve, central bank policy, Brexit, and geo-political challenges around the globe. While these headlines grab our attention it’s important to recognize the underlying economic fundamentals that lead us to believe that the economy is on a steady path and that a recession is not imminent.

Much of the volatility seen in US stocks this year can also be found in other parts of the market as international stocks struggled (with the MSCI World ex-US down 14%), bonds drifted downward (the Barclays US Aggregate bond index down a little less than 1%), and precious metals also struggled (gold down about 5%) all through December 14th (YCharts, LPL Financial). Uncertainty weighed on investor sentiment for much of 2018 and many of these uncertainties could continue into 2019. The following commentary is going to discuss many of the uncertainties we feel will be significant next year alongside our fundamental outlook for the economy.

Here are some of the highlights:

- The economic cycle continues to age, but we believe the US economy remains on firm footing.

- Opportunities might be found internationally as foreign stock market valuations appear to show attractive valuations, while economic growth could stabilize if we see progress on trade, Brexit, and other geo-political uncertainties.

- Growth in corporate earnings appears set to continue after an excellent 2018.

- The trade dispute between the US and China will take center stage as the impact of tariffs and conflict between the world’s two largest economies drags on.

- The UK continues to struggle with Brexit – 2019 may determine what their relationship with the EU will look like moving forward.

- The Federal Reserve is likely to continue to hike rates in 2019, although it’s likely to raise rates fewer times than we saw in 2018 (4).

- Interest Rates will be watched closely as part of the yield curve inverted toward the end of 2018 – will the more significant portion of the yield curve invert in 2019?

The Uncertainties:

Trade: the trade war between the US and China, the world’s two largest economies, escalated throughout 2018 starting with the US implementing tariffs on solar panels and washing machines in February and expanding to various retaliatory tariffs across a wide spectrum of industries. Investors read between the lines on every comment, statement, and action by leaders from both nations to determine if a resolution was forthcoming. Trump and Xi’s meeting on December 1st marked the beginning of a 90-day truce that ends on March 1st. Both sides are working in earnest to continue negotiations as there is a lot to lose. The longer the trade war continues the costlier the tariffs become as the impact on consumer and business confidence worsens. A resolution to trade (which we believe is in the best interests of each nation) would likely provide a boost to stocks and allow businesses to focus on the future with a solid understanding of what the trade rules will look like moving forward. That is an environment in which we’d expect to see business spending pick up and international stocks (that are more trade dependent) do well.

The Federal Reserve: Fed Chair Jay Powell took the reigns of the Fed at the beginning of 2018 and has learned firsthand the importance of communication as investors analyze his every word in an effort to determine the Fed’s outlook. The Fed raised rates 4 times in 2018 as the economy strengthened, unemployment remained at low levels, and we began to see some signs of inflation. Concerns that the Fed has been raising rates too quickly emerged throughout the year; however, the Fed has tried to manage those expectations over the last couple of months by assuring investors they continue to be data dependent and are not on a pre-set path. Many investors now feel it’s likely the Fed will only raise rates once or twice in 2019. (CME FedWatch tool). We continue to believe that the Fed has been raising rates as a result of a growing and steady US economy (a good reason), but need to be careful as the risk of a central bank mistake increases the later we move in the economic cycle.

Washington: Midterms are now firmly in the rearview mirror. Questions linger about how (if at all) the split Congress will work together over the next couple of years. We think it’s unlikely we’ll see much agreement, and as such major legislative changes are unlikely. This will likely leave in place economic policies that gave stocks a boost over the last two years: tax reform and de-regulation.

Brexit: If you are frustrated with politics and disagreement here in the US, then imagine being in the United Kingdom (UK). The UK’s Brexit from the European Union (EU) has been contentious between the UK and the EU, and within the UK. The two sides have struggled to come to any agreement on how to part ways. The UK is officially scheduled to leave the EU on March 29th, 2019 with a 21-month transition period stretching to the end of 2020. The uncertainty surrounding next steps will continue to weigh on investors until some sort of resolution is found.

The Fundamentals:

We believe that economic fundamentals present a strong indication that there is not a recession on the near-term horizon for the US with GDP growth projected at 2.7% for 2019 (OECD). Globally, we are a little more cautious as there are some potential headwinds (trade, Brexit, geo-political risk) particularly in Europe and China. Growth globally is projected at 3.5%, while Europe’s growth is projected to slow to 1.7% from 1.9% in 2018 (OECD).

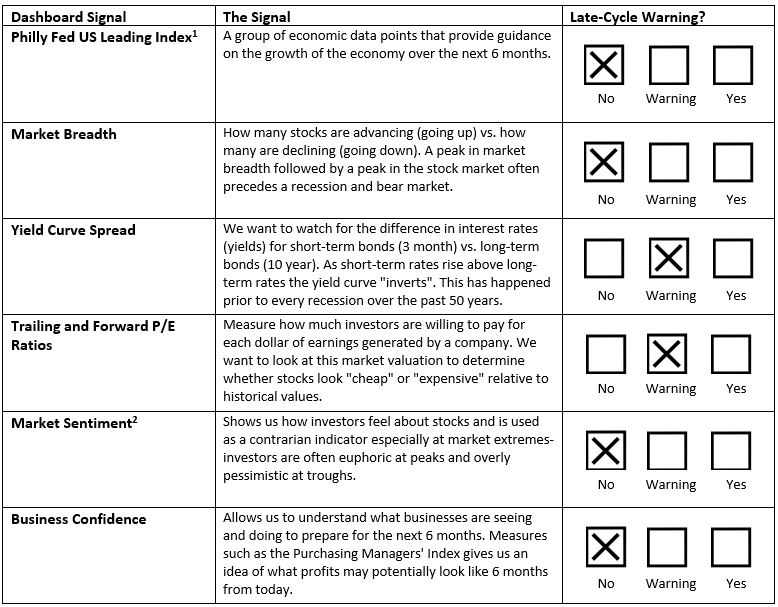

We regularly review and update our economic dashboard, which consists of 6 indicators that have historically been good signals ahead of a recession. The current standing of the dashboard reinforces our view that a recession in the US is unlikely as we move into 2019. Last year we highlighted two areas that we felt were beginning to concern us: one of those, valuations, has improved over the last 12 months while another, the yield curve, has become more concerning. Here is a look at the dashboard in full with some additional commentary on these data points.

Yield Curve & Interest Rates: 2018 has seen interest rates move higher across the board as the economy has strengthened and we’ve started to see some beginning signs of inflation. In our dashboard we watch the yield spread, the difference in yield between the 10-year Treasury and the 3-month Treasury Bill. This indicator has historically signaled a recession over the next 12 months once the yield curve inverts (the 10-year yields less than the 3-month). While both 10 year and 3-month yields have risen over the year the difference (the spread) between the two has shrunk moving us closer to an inversion in the curve. Recently, many investors were concerned when we saw an inversion of a different part of the yield curve (5-year vs. 3-year); however, this inversion does not have a historically strong track record of signaling a recession. We will continue to watch interest rates closely as a yield curve inversion would be a significant sign that a recession is more likely in the years to come. That said, an inversion of the yield curve is not a good market timing device: the last 5 times the yield curve has inverted stocks have risen an average of 21.8% before reaching a peak (LPL Financial).

Valuations: At this time last year we noted that US stocks looked expensive when compared to their long-term average, but that may have been justified given low interest rates at that time. Looking at valuations now compared to last year stocks appear much more attractive as stock prices are little moved while earnings are on track to grow over 20% in 2018 (FactSet). P/E ratios (price divided by earnings), a fairly common measure of stock valuations, have dropped substantially since this time last year. Today’s trailing 12-month P/E is 17.76 (through Q3 earnings) versus 21.21 last year. Forward looking valuations also look more attractive with the forward 12-month P/E at 15.4, which is now below the 5-year average of 16.4 (FactSet). We also believe that valuations appear more attractive internationally providing a strong reason to invest globally, despite concerns of slowing global growth.

Earnings: Perhaps the most positive economic story of 2018 can be found in earnings growth. S&P 500 earnings are expected to post annual growth of over 20% with only the 4th quarter’s earnings left to report. As detailed above, this robust earnings growth has not driven stocks higher as valuations have contracted. Moving into 2019 earnings forecasts are for continued growth with analysts projecting earnings growth of almost 9%, and revenue growth of roughly 6% for the S&P 500 (Factset). Earnings growth has historically been a strong driver of stock market returns, and could be a positive factor as we look toward next year.

Asset Allocation & Financial Planning

The TLWM outlook is that the risk of recession is fairly low which means we want to remain fully invested in our equity portfolios as we expect to see positive stock market returns. We see some signs of potential slowing economic growth in international economies, but attractive valuations alongside positive earnings growth potentially provides good opportunities for growth and diversification and as such we want to maintain some international exposure within portfolios.

We continue to get later in the economic cycle and that has often meant more volatility (as we’ve seen this year!). Be prepared for volatility to continue into 2019. The uncertainties we discussed earlier (Brexit, trade, central bank policy, etc..) are likely to be major factors that have the potential to move markets. This can be seen maybe most clearly in trade: if we see a positive resolution a great deal of uncertainty would be removed and should allow businesses to make plans with a better understanding of the playing field moving forward. These uncertainties and heightened stock market volatility have us on the lookout and we stand ready to make changes to our portfolio allocation as needed.

Last year we warned of not abandoning your long-term asset allocation as investors wondered whether it was time to reduce their fixed income exposure and look for more growth given the strong and steady stock market in 2017. This year, concerns about the market have caused some to ask whether it’s time to make the opposite change? While volatility (up and down) can make investors worry about missing out on the upside, or experiencing too much downside we feel it’s important to remind you that we work carefully with each one of you to determine an asset allocation that aims to maximize the chances of meeting your goals and objectives while keeping in mind risk tolerance, time horizon, and income needs. Our financial planning process allows us to ensure we leave no stone unturned, determine a purpose for every dollar, and keep our focus on how best to achieve your long-term goals and objectives.

We wish all of you a wonderful holiday season and happy and health New Year.

*Investment advice offered through TLWM, LLC., a registered investment advisor.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged index. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following developed country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK.

*Investing in foreign securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

*Credit risk can be a factor in situations where an investment’s performance relies on a borrower’s repayment of borrowed funds. With credit risk, an investor can experience a loss or unfavorable performance if a borrower does not repay the borrowed funds as expected or required. Investment holdings that involve forms of indebtedness (i.e. borrowed funds) are subject to credit risk.

* Typically, the values of fixed-income securities change inversely with prevailing interest rates. Therefore, a fundamental risk of fixed-income securities is interest rate risk, which is the risk that their value will generally decline as prevailing interest rates rise, which may cause your account value to likewise decrease, and vice versa. How specific fixed income securities may react to changes in interest rates will depend on the specific characteristics of each security. Fixed-income securities are also subject to credit risk, prepayment risk, valuation risk, and liquidity risk. Credit risk is the chance that a bond issuer will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of a bond to decline.

* The price-earnings ratio (P/E Ratio) is the ratio for valuing a company that measures its current share price relative to its per-share earnings.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Consult your financial professional before making any investment decision.

* Stock investing involves risk including loss of principal.

* This document is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Texas Legacy Wealth Management and its representatives are properly licensed or exempt from licensure.

1 These Leading Indices predict each state's coincident index growth rate for six months. Estimates are based on a vector autoregression model along with state-level housing permits, initial claims for unemployment insurance, delivery times from the ISM manufacturing survey, and interest rate spreads between 3-month and 10-year treasuries. There is also a US national prediction. (YCHARTS)

2 The small business optimism index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members. The index is a composite of 10 seasonally adjusted components based on the following questions: plans to increase employment, plans to make capital outlays, plans to increase inventories, expect economy to improve, expect real sales higher, current inventory, current job openings, expected credit conditions, now a good time to expand, and earnings trend. (Bloomberg)