Mid-Year Outlook 2017

Submitted by TLWM Financial on June 28th, 2017The first half of 2017 is in the books, and what a great start to the year it has been with the S&P 500 rallying about 8% (seen in the chart below), lead by the technology and healthcare sectors. While news headlines have created a constant distraction, particularly on the political front, the stock market has been steady as evidenced by remarkably low volatility[1]. A quiet market is one to be enjoyed, as stocks tend to drift higher in that environment; however, we would not be surprised to see an increase in volatility during the second half of the year.

Fundamentally, we've seen steady economic data, strong corporate earnings and optimistic investor sentiment. Internationally, fundamentals have improved as well. The improvement in economic data overseas combined with attractive equity valuations has led to strong returns for international stocks. As we look to the rest of 2017, we remain positive on the market and continue to be fully invested as we don't see a recession on the horizon.

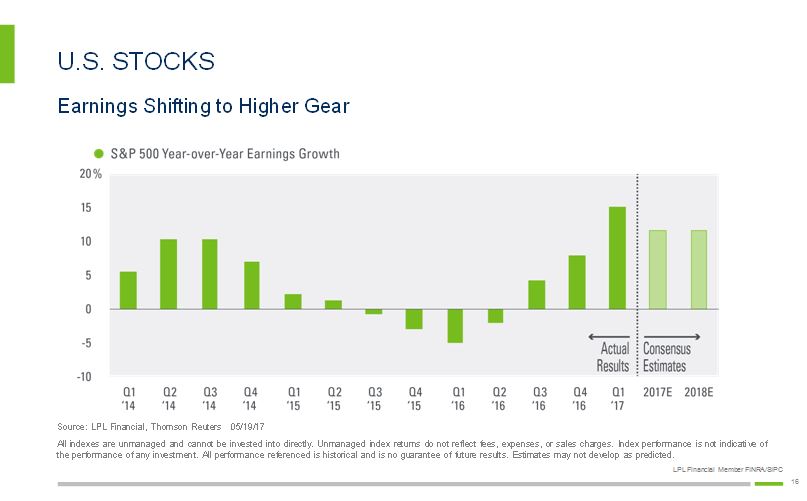

A common concern for investors (and one that we hear from clients) is whether or not stocks are simply too expensive. The argument is made that stocks are at all time highs - can they possibly go higher? While the stock market is a little more expensive than historic averages, P/E's (one measure of how expensive stocks are) have actually become a little less expensive as earnings (and earnings estimates) have increased, potentially justifying higher prices. In first quarter 2017, the S&P 500 had year over year earnings growth just north of 15% which was the best quarter since 2011, according to LPL Research. Earnings estimates continue to look good for the rest of 2017 and 2018, with growth estimates of approximately 10% over the next 12 months (LPL Research). Strong earnings growth shows that corporations continue to perform well in the current environment. We could see even further improvement in the current economic and earnings environment if the much discussed fiscal policy gets enacted. A boost in growth could potentially support stocks moving higher; however, we would also note that political uncertainty remains and leaves potential for increased volatility if fiscal actions disappoint investors.

Turning to monetary policy, central banks around the world continue on divergent paths as the Fed continues to tighten here in the US while other central banks appear to be more accommodative. In June, the Fed raised interest rates for the fourth time in the current tightening cycle and announced a plan to begin reducing their balance sheet. - In our opinion, this is a sign that the Fed seems optimistic about the direction of the US economy moving forward. That said, they also reaffirmed that the pace of rate hikes moving forward will likely be gradual which potentially bodes well for stocks. Looking overseas, more accommodative policy (particularly in Europe) gives additional reason for international exposure as it appears many areas of the globe may be a little earlier in the economic cycle than the US. Monetary policy could continue to put pressure on interest rates, which may make bonds look expensive. While bonds may appear a little more expensive than normal, fixed income still plays a critical role in asset allocation, as a well diversified portfolio will potentially help reduce volatility.

Our overall outlook for the rest of the year remains positive as we are optimistic on fundamental economic data, corporate earnings and the labor market, and therefore we remain fully allocated. We do not see a recession over the next 6-9 months, but wouldn't be surprised to see volatility pick-up as political uncertainty has the potential to weigh on investors. As always, we will continue to monitor the economy and market and stand ready to make changes within the portfolios.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged index. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Consult your financial professional before making any investment decision.

* Stock investing involves risk including loss of principal.

* This document is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Texas Legacy Wealth Management and its representatives are properly licensed or exempt from licensure.

* International and emerging market investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

*Portions of this material were prepared by LPL Financial.

*There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification and asset allocation do not protect against market risk.

*Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price