Monthly Market Update

Submitted by TLWM Financial on April 30th, 2019Another steady month for stocks in March brought the first quarter to a close with the S&P 500 rallying about 13% over the first three months of the year while international stocks also performed well closing the quarter up about 9.5% (MSCI World ex-US, YCharts), albeit both still down from their all-time highs. We are encouraged by the continued recovery of the stock market this year; however, we continue to monitor a number of uncertainties including trade and Brexit along with our economic dashboard.

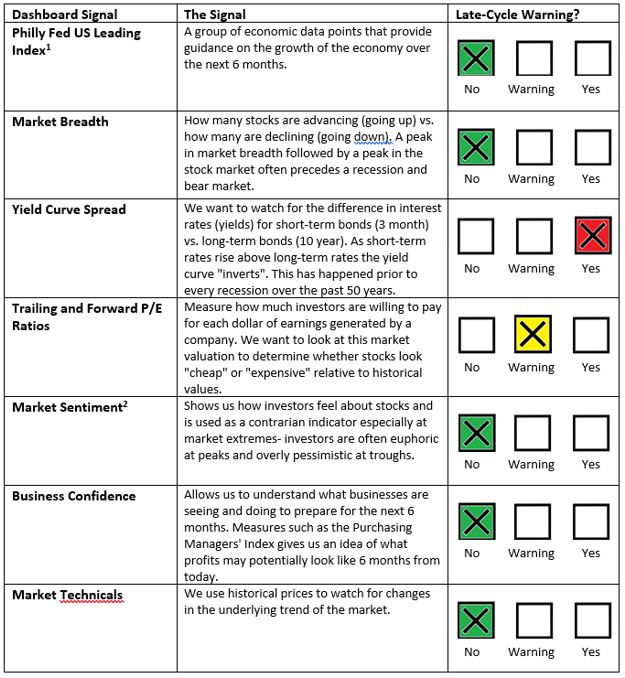

Our economic dashboard, which consists of indicators that have historically been good signals ahead of a recession, is currently sending mixed signals. Recently, the yield curve spread indicator triggered as the yield curve inverted (which happens when short-term rates move above long-term rates). This change resulted in a downgrade to red from yellow, while at the same time recent market strength has led us to upgrade our technical indicator to green. While these conflicting signs may seem confusing it’s important to note that although an inversion in the yield curve has historically been a good indicator of a recession, it has not been a good timing indicator. We feel that the inverted yield curve potentially signals an increase in the odds of a recession in the years to come, but does not signal that a recession is imminent. In fact, the US economy has historically peaked an average of 16 months after an initial yield curve inversion (LPL Financial). Therefore, we are not making any immediate changes to the portfolio and remain fully allocated at this time.

Our short to intermediate term outlook is still positive but we are more cautious looking out beyond 12 months as we believe the chance of recession has increased. We will continue to watch our dashboard, economic data, trade, Brexit and other geopolitical events very closely and stand ready to make changes to portfolios when needed.

Please find our economic dashboard below:

[1] These Leading Indices predict each state's coincident index growth rate for six months. Estimates are based on a vector autoregression model along with state-level housing permits, initial claims for unemployment insurance, delivery times from the ISM manufacturing survey, and interest rate spreads between 3-month and 10-year treasuries. There is also a US national prediction. (YCHARTS)

2 The small business optimism index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members. The index is a composite of 10 seasonally adjusted components based on the following questions: plans to increase employment, plans to make capital outlays, plans to increase inventories, expect economy to improve, expect real sales higher, current inventory, current job openings, expected credit conditions, now a good time to expand, and earnings trend. (Bloomberg)

Sincerely,

Your TLWM Team

*Investment advice offered through TLWM, LLC., a registered investment advisor.

*The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

*The Standard & Poor’s 500 (S&P 500) is an unmanaged index. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

*The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following developed country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the UK.

*Investing in foreign securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

*The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

*Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

*Typically, the values of fixed-income securities change inversely with prevailing interest rates. Therefore, a fundamental risk of fixed-income securities is interest rate risk, which is the risk that their value will generally decline as prevailing interest rates rise, which may cause your account value to likewise decrease, and vice versa. How specific fixed income securities may react to changes in interest rates will depend on the specific characteristics of each security. Fixed-income securities are also subject to credit risk, prepayment risk, valuation risk, and liquidity risk. Credit risk is the chance that a bond issuer will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of a bond to decline.