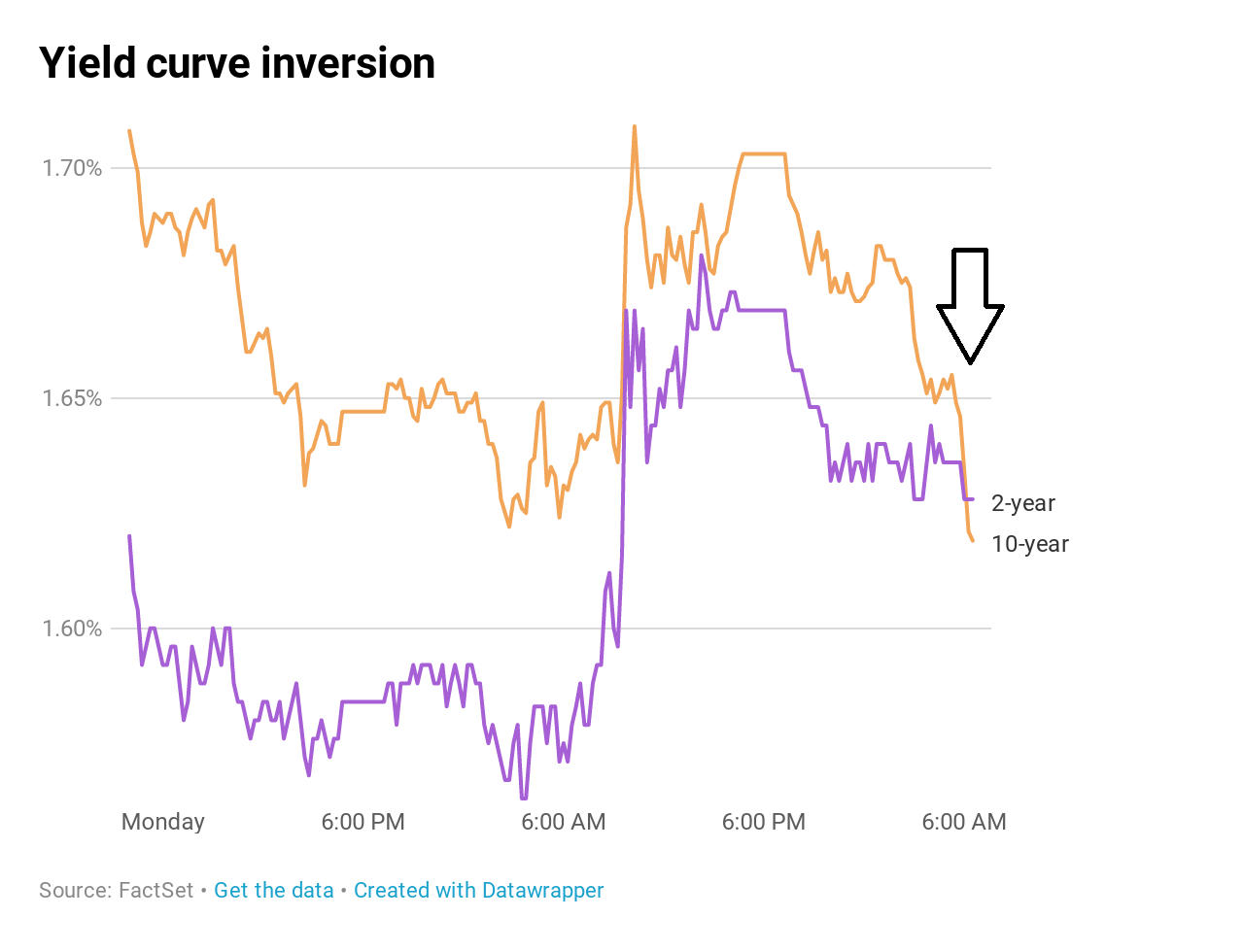

Yield Curve

Submitted by TLWM Financial on August 14th, 2019On 8.14.19, a closely-watched recession signal flashed red with the inversion of the 10YR-2YR US Treasury yield curve, another part of the yield curve to invert. An inversion of the yield curve means that long-term rates are lower than shorter term rates (in this case the 10-year US Treasury vs the 2-year US Treasury). This has led many in the financial media to announce that a recession is inevitable. While we watch the 10yr-3month yield curve on our economic dashboard, this is just a further warning sign we will be watching carefully as we get longer in the economic cycle.

Source: CNBC

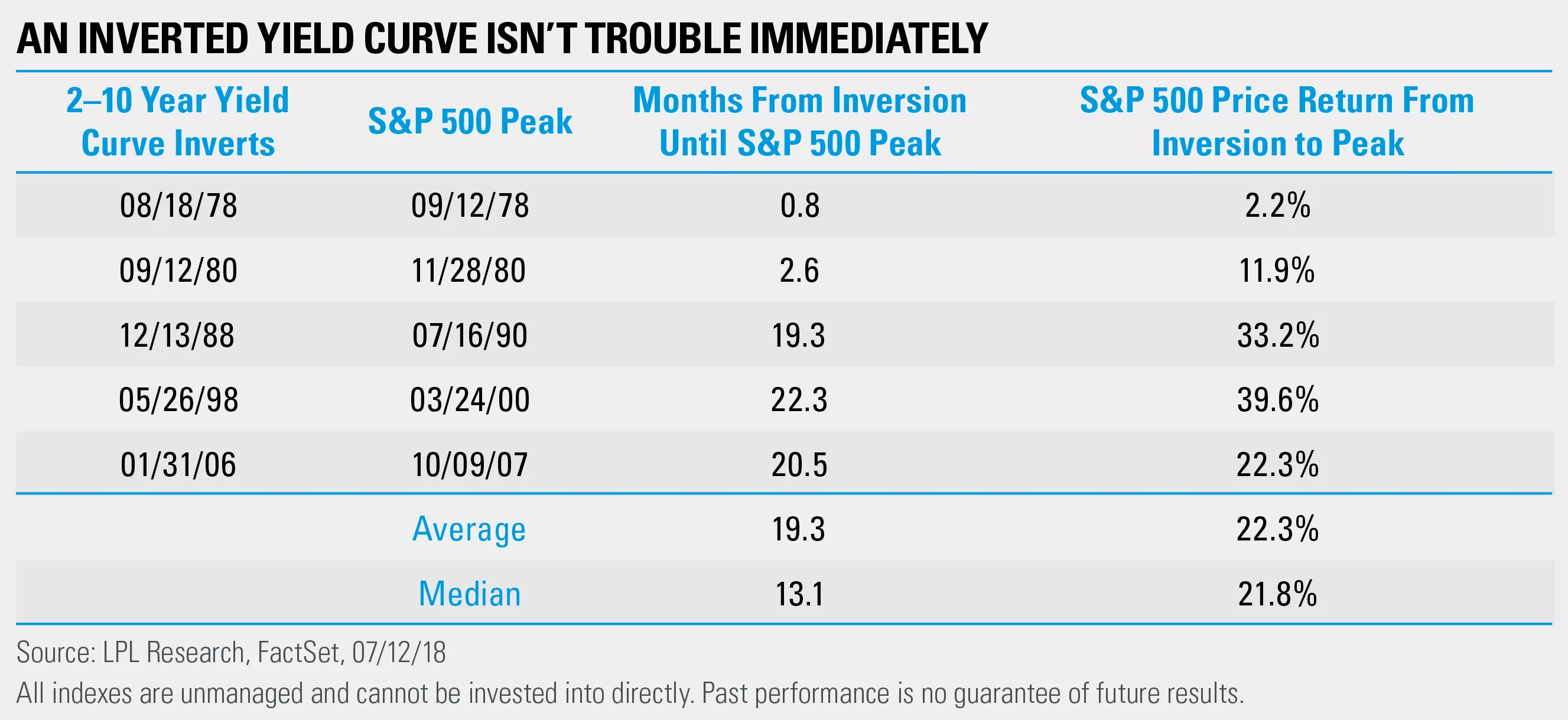

An inversion is seen as a potential symptom of a sick economy and has generally been a reliable indicator of a recession; however, the inversion of the yield curve has not historically been a good timing indicator. In fact, a recession occurs, on average 22 months following an inversion of the 10-2 yr yield curve (Credit Suisse, CNBC), while stocks have often continued to move higher as can be seen in the chart below:

We agree that the inversion of the yield curve is a troubling sign, and is currently the only data point in our economic dashboard flashing red. We will continue to monitor economic data along with other major risks including the ongoing trade war, Brexit, central bank policy, and other geo-political risks such as the recent Hong Kong protests. While we believe the economy is unlikely to move into a recession immediately, we do feel that there are increased risks of a recession looking out beyond this year, and we stand ready to make changes to portfolios as needed.

*Investment advice offered through TLWM, LLC., a registered investment advisor.

* The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. You cannot invest directly in this index.

* The Standard & Poor’s 500 (S&P 500) is an unmanaged index. Unmanaged index returns do not reflect fees, expenses, or sales charges. Index performance is not indicative of the performance of any investment.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

* Economic forecasts set forth may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Past performance does not guarantee future results. Investing involves risk, including loss of principal.

* You cannot invest directly in an index.

* Consult your financial professional before making any investment decision.

* Stock investing involves risk including loss of principal.

* This document is solely for informational purposes. Advisory services are only offered to clients or prospective clients where Texas Legacy Wealth Management and its representatives are properly licensed or exempt from licensure.

* The 10-year Treasury Note represents debt owed by the United States Treasury to the public. Since the U.S. Government is seen as a risk-free borrower, investors use the 10-year Treasury Note as a benchmark for the long-term bond market.

* Government bonds and Treasury Bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

* Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

*Credit risk can be a factor in situations where an investment’s performance relies on a borrower’s repayment of borrowed funds. With credit risk, an investor can experience a loss or unfavorable performance if a borrower does not repay the borrowed funds as expected or required. Investment holdings that involve forms of indebtedness (i.e. borrowed funds) are subject to credit risk.

* Typically, the values of fixed-income securities change inversely with prevailing interest rates. Therefore, a fundamental risk of fixed-income securities is interest rate risk, which is the risk that their value will generally decline as prevailing interest rates rise, which may cause your account value to likewise decrease, and vice versa. How specific fixed income securities may react to changes in interest rates will depend on the specific characteristics of each security. Fixed-income securities are also subject to credit risk, prepayment risk, valuation risk, and liquidity risk. Credit risk is the chance that a bond issuer will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of a bond to decline.